EBITDA is an acronym, short for “Earnings Before Interest, Taxes, Depreciation, and Amortization.” It is calculated by taking net income and adding back income taxes, interest expense, depreciation, and amortization. Publicly traded companies and closely held businesses alike use EBITDA, often (sometimes controversially) adjusted, in performance evaluation and communication, M&A and business valuation, compensation programs, and other parts of their business. An example of the calculation of EBITDA using reported financial information might look like this:

While not a financial measure explicitly recognized under generally accepted accounting principles (GAAP) (i.e., there is no accounting standard about it), EBITDA is one of the most widely used metrics in finance—particularly when it comes to financial analysis, debt underwriting and covenants, and business valuation. At a fundamental level, there are three broad buckets of factors that drive the value of any business: company performance (e.g., revenue, EBITDA margins, net income, etc.), company growth expectations, and the underlying riskiness in expected continued company performance and growth. EBITDA is a key metric used by acquirers, investment bankers, financial analysts, accountants, and many others in developing a perspective on company performance and profitability, an idea of a company’s cash flow potential, and a benchmark useful for evaluating and underwriting the risk of expected growth and performance. Therefore, understanding what EBITDA is, how EBITDA is calculated, and how third parties might view or use EBITDA is of critical importance for business owners and management teams.

Why the Focus on EBITDA?

As a metric, EBITDA first came to prominence in the mid-1980s, when a number of CEOs felt that net income didn’t properly reflect ongoing earnings quality or expected cash flow due to interest charges and/or depreciation related to major capital expenditures. EBITDA’s rise to prominence also happened around the same time that investors were starting to utilize the leveraged buy-out as a means of acquiring businesses perceived to be undervalued (likely due in part to predecessor owner/investor reliance on “outdated” net income). Its proponents argue that EBITDA offers a clearer reflection of operations by stripping out capital structure choices (debt versus equity financing), choices related to how an entity is taxed (pass through or entity level), or how management allocates the basis of acquired tangible and intangible assets to future periods (through depreciation and amortization) that can obscure how the company is really performing. EBITDA focuses solely on operating expenses including cost of services/goods sold, sales and marketing expenses, and general and administrative expenses. In theory, EBITDA should provide a view of the gross-of-tax return on total capital invested for any given period.

Stripping out these types of expenses can also be useful when analyzing a company or when comparing businesses across an industry. For example, if during the M&A process, the acquiring company would likely change the capital structure of the target company (i.e., the mix of debt and equity used to finance the business), analyzing the company’s earnings prior to interest expense would be prudent. Additionally, under current GAAP, nearly any acquisition contemplated is likely to result in an increase in amortization expense due to the step up in the value of intangible assets (and perhaps goodwill) acquired. Such amortization expense fundamentally changes little about the company’s earnings capacity, suggesting that analyzing income before amortization is a worthwhile endeavor. Similar issues arise related to tangible long-lived assets and depreciation policy: a building being depreciated perhaps has increased in value and has not depreciated at all. All these factors were identified by financial analysts and investors as potentially distorting the true performance and profitability of businesses, thus meriting the calculation and use of EBITDA.

EBITDA is the Starting Point

By isolating a certain subset of costs, EBITDA does a good job measuring operational performance. Yet, EBITDA should not be used blindly as an alternative for free cash flow. In some industries, the very expenses that EBITDA excludes are fundamental (and very real) expenses required in the day-to-day operations of the company. For companies in capital-intensive industries such as manufacturing or shipping, depreciation is a major expense category and cannot be ignored, as routine capital expenditure is necessary for maintaining and growing operations. While EBITDA can be used (with care) as a proxy for cash flow in small service-based businesses, EBITDA is best viewed as the highest level of cash flow that is available (or not) for all of the reinvestments that are necessary to meet the needs of the business and to provide returns for owners.

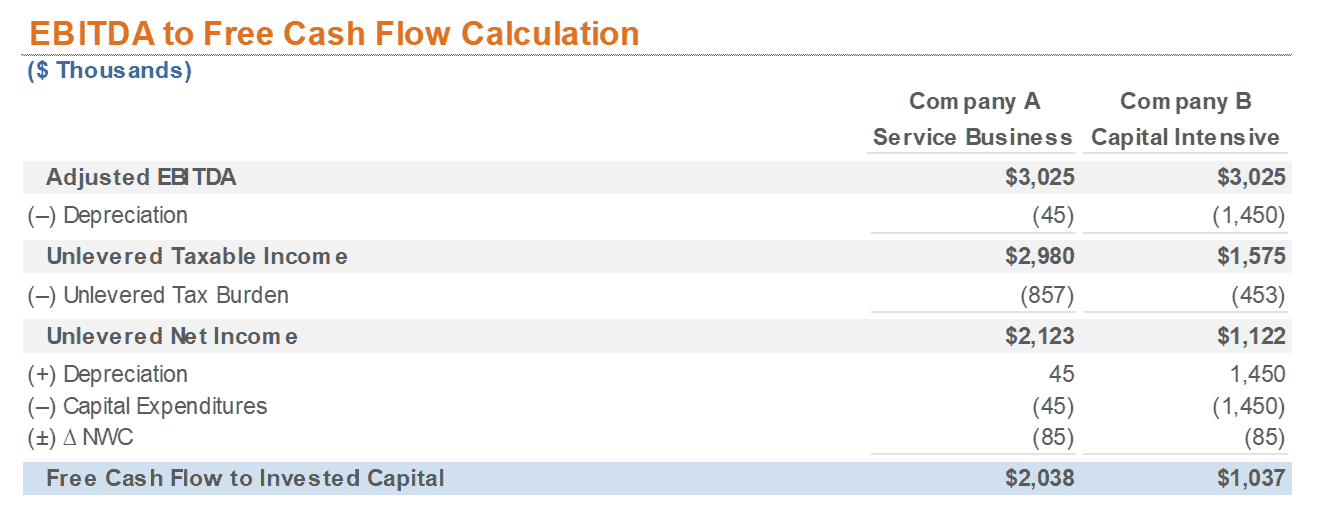

The chart below shows the relationship between EBITDA and free cash flow to invested capital—which is defined as the cash flow-generating capacity of a business prior to consideration of how it may be financed, also known as unlevered free cash flow. Company A is a service business that has low capital expenditure requirements, while Company B is a capital-intensive business that has significant ongoing fixed asset needs.

Since both businesses have equal EBITDA figures, we might conclude that the companies have similar investment characteristics. However, by converting from EBITDA to free cash flow to invested capital, we arrive at a different conclusion. In this example, Company A generates significantly more cash flow than Company B, because ongoing fixed asset purchases represent such a large portion of Company B’s cash outflows.

Helping You Get There…

The focus on EBITDA is clear. Corporate acquirers, private equity investors, investment bankers, financial analysts, and other market participants all focus on this important financial metric. As a result, businesses should be focused on improving EBITDA and EBITDA margins, because all else equal, the higher EBITDA, the higher the value of the business. However, this metric should be used in tandem with other earning measures, such as free cash flows, to fully understand the earning capacity of the business.

To learn more about how EBITDA drives much of the value of your business, please connect with a member of Boulay’s Transaction Group.