The Small Business Administration

Defined as independent businesses having fewer than 500 employees, there are more than 32 million small businesses in America. Combined, small businesses account for 99.9% of all U.S. businesses and support more than 60 million jobs. So, in terms of their impact on the economy, small businesses aren’t actually that small.

Established in 1953 with President Eisenhower’s signing of the Small Business Act, the U.S. Small Business Administration (SBA) is the only cabinet-level federal agency fully dedicated to small business. Through an extensive network of field offices and partnerships with public and private organizations, the SBA delivers its services throughout the U.S. Since its founding, the SBA has delivered millions of loans, loan guarantees, contract certifications, counseling sessions, disaster loans, and other forms of support to small businesses.

SBA Loans

The SBA was created to help ensure that small businesses have the tools and resources they need to start and expand their operations and create jobs that support a growing economy and strong middle class. One key area in which the SBA helps small businesses is through SBA-backed loans.

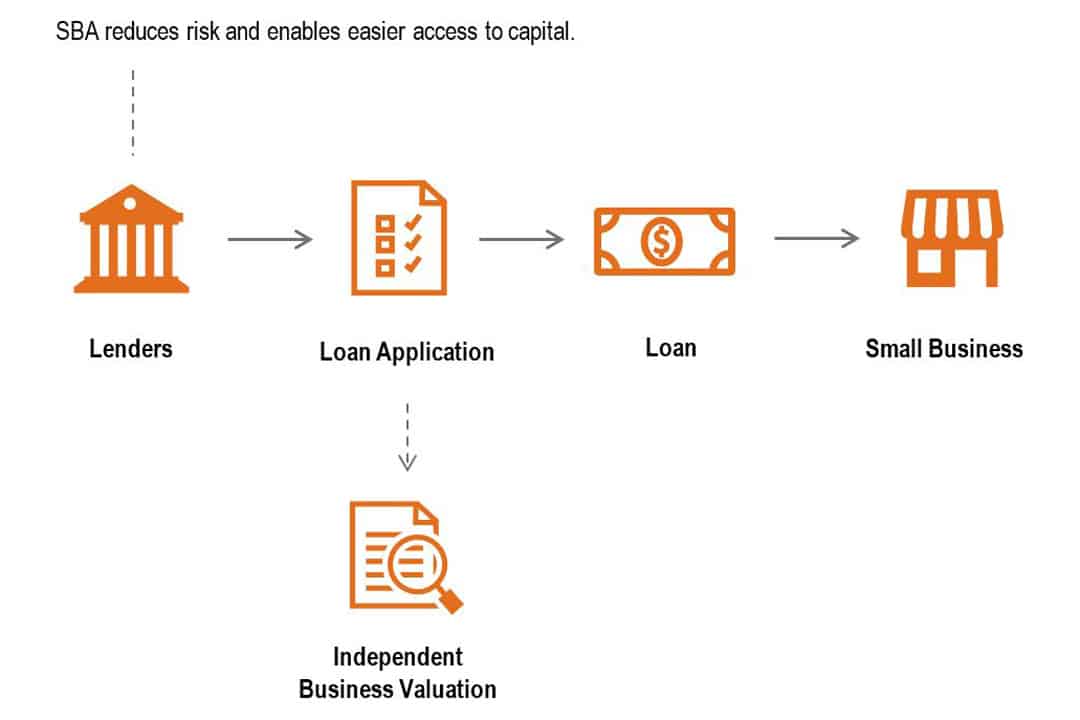

Access to capital is critical to the long-term success of small businesses. Many entrepreneurs do not have the same access to credit as larger businesses that can more readily take on a traditional loan from a bank, or new entrepreneurs may not have a credit score that can guarantee them a loan. In addition, underserved small businesses are more likely to be denied credit and must rely on personal savings or credit cards to sustain their business. The SBA works to fill gaps in commercial lending markets so that small businesses across the U.S. can access credit on reasonable commercial terms.

SBA loans help small businesses get funding by setting guidelines for loans and reducing lender risk. SBA loans are made through private banks, credit unions, or other lenders who partner with the SBA to ensure all entrepreneurs have access to capital to start and grow their business.

SBA-guaranteed loans have several benefits:

- Competitive terms: SBA-guaranteed loans generally have rates and fees that are comparable to non-guaranteed loans

- Counseling and education: Some loans come with continued support to help small business owners start and run their business

- Unique benefits: Lower down payments, flexible overhead requirements, and no collateral needed for some loans

There are three distinct types of SBA loans:

- 7(a) loans – The 7(a) Loan Program is the SBA’s most common loan program. The maximum loan amount for a 7(a) loan is $5 million and key eligibility factors are based on what the business does to receive its income, its credit history, and where the business operates. This is the best option when real estate is part of a business purchase, but it can also be used for:

- Short- and long-term working capital

- Refinancing current business debt

- Purchasing furniture, fixtures, and supplies

- 7(a) loans – The 7(a) Loan Program is the SBA’s most common loan program. The maximum loan amount for a 7(a) loan is $5 million and key eligibility factors are based on what the business does to receive its income, its credit history, and where the business operates. This is the best option when real estate is part of a business purchase, but it can also be used for:

- 504 loans – The CDC/504 Loan Program provides long-term, fixed rate financing for major fixed assets that promote business growth and job creation. The maximum loan amount for a 504 loan is $5 million. 504 loans are available through Certified Development Companies (CDCs), SBA’s community-based partners who regulate nonprofits and promote economic development within their communities. CDCs are certified and regulated by the SBA

- Microloans – The microloan program provides loans up to $50,000 to help small businesses rebuild, re-open, repair, enhance, or improve, but proceeds cannot be used to pay existing debts or to purchase real estate

When is an Independent Business Valuation Required for an SBA Loan?

SBA loans are a great way for small businesses to obtain financing, but it is important that all involved parties understand when an independent business valuation is required, who is qualified to prepare them, and the specific guidelines valuation analysts must follow when preparing them.

The SBA sets the guidelines that govern the 7(a) and 504 loan programs. These guidelines determine which businesses SBA Lenders (e.g., banks, credit unions, CDCs) can lend to and the type of loans that they can give. Since SBA loans are partly guaranteed by the SBA, participating lenders are required to obtain an independent business valuation from a qualified source if:

- The amount being financed (including any combination of 7(a), 504, seller or other financing)—excluding the appraised value of real estate and/or equipment—is greater than $250,000

- There is a close relationship between the buyer and seller (e.g., transactions between family members or business partners)

- The lender’s internal policies and procedures require an independent business valuation from a qualified source

With respect to business valuations, a “qualified source” is an individual who regularly receives compensation for business valuations and is accredited by one of the following recognized organizations:

- Accredited in Business Valuation (ABV) accredited through the American Institute of Certified Public Accountants;

- Accredited Senior Appraiser (ASA) accredited through the American Society of Appraisers;

- Certified Valuation Analyst (CVA) accredited through the National Association of Certified Valuation Analysts;

- Certified Business Appraiser (CBA) accredited through the Institute of Business Appraisers; and

- Business Certified Appraiser (BCA) accredited through the International Society of Business Appraisers

When a business valuation is required for SBA lending purposes, additional requirements include:

- The business valuation must be requested by, and prepared for, the lender. The lender may not use a business valuation prepared for the applicant or the seller

- The scope of work should identify whether the transaction is an asset purchase or stock purchase and be specific enough for the valuation analyst to know what is included in the sale (including any assumed debt)

- The business valuation must include the valuation analyst’s conclusion of value, professional qualifications, and signature certifying to the information contained in the valuation

- The business valuation must be conducted in compliance with the current Uniform Standards of Professional Appraisal Practice (USPAP) guidelines

Helping you get there…

The Boulay Transaction Group offers business valuation services for a variety of purposes, including SBA lending. In addition to business valuations, we offer buy- and sell-side due diligence, quality of earnings analysis, transaction structuring, divorce financial services and more. To learn more about how we support you at every stage of your transaction, connect with a member of the Boulay Transaction Group today.