For many people, planning for retirement may feel like navigating to a far-off destination with no map packed. There’s a clear end goal in mind, but winding paths and obstacles may make the journey more difficult than it needs to be. Fortunately, many employers offer certain benefits that help their employees navigate this journey and successfully reach their retirement destination.

One commonly offered benefit is an employer 401(k) plan. As employers set up a 401(k) for their employees, there are many different avenues, approaches and investment products to consider. One type of investment product, the Target-Date Fund (TDF), allows an employee’s 401(k) to move and shift in tandem with their target year of retirement. TDFs help ensure an employee’s 401(k) is more responsive to changes in their risk tolerance and the market as retirement approaches.

If you’re considering including TDFs in your employer 401(k) plan investment lineup, there are a few key details you need to know regarding which glide path to follow.

The Basics of TDFs

At its core, a TDF provides a straightforward investment strategy. Investors select a fund with a target date aligned with their expected retirement year, such as 2030 or 2055. Over time, the fund manager adjusts the portfolio, balancing allocations between stocks, bonds, and other assets based on the investor’s changing risk tolerance as retirement approaches. While they might seem standardized due to their target-year nomenclature, TDFs can vary significantly in how they achieve their objectives.

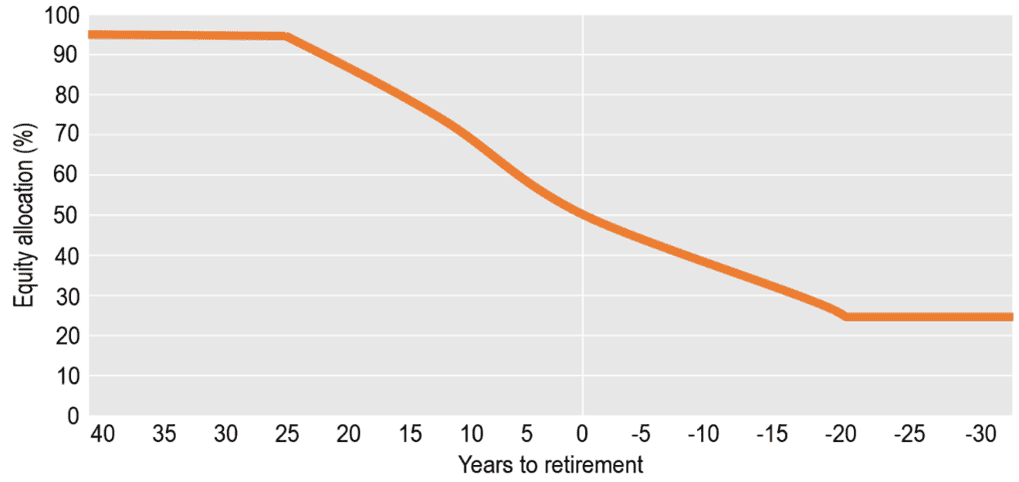

Understanding the Glide Path

The central element that distinguishes one TDF from another is its glide path. The glide path outlines the fund’s prescribed asset allocation adjustments as an investor ages, striking a balance between growth potential and risk management. In the early and middle stages of an investor’s career, when retirement is still decades away, TDFs typically maintain a high equity exposure of 80 to 90 percent of the portfolio, with the remainder in bonds. As the target retirement date draws closer, this allocation gradually shifts to 70 to 80 percent in equities when retirement is a couple of decades away, and eventually, 40 to 55 percent at retirement.

The rationale behind this changing equity exposure is rooted in the historical outperformance of stocks compared to bonds over the long term. Younger investors are better positioned to weather market downturns compared to those nearing retirement, as they have more time to recover from volatility.

“Through” and “To” Glide Paths

Upon reaching the target retirement date, TDFs adopt one of two approaches. “Through” glide paths continue to adjust asset allocation for the first 10 to 20 years of retirement, with equity allocations ranging from 25 to 50 percent. This strategy aims to cater to investors with longer life expectancies, helping them address the risk of outliving their savings.

In contrast, “to” glide paths maintain a static asset allocation post-retirement, resulting in a flat line on the glide path chart. This approach acknowledges retirement as a decision point, allowing investors to transfer TDF assets into other vehicles designed for retirees, such as individual retirement accounts (IRAs) or unified accounts managed by financial professionals.

Choosing the Right TDF

As a Plan Sponsor, selecting the appropriate group of TDFs for your 401(k) plan participants involves understanding the fund manager’s glide path design and philosophy. Additionally, factors like manager tenure, industry ratings, risk-adjusted performance, and the manager’s personal investment in the funds they manage should be considered.

It is crucial to provide participants with the education and guidance they need to comprehend TDFs, grasp how glide paths function, and integrate them into their personalized retirement strategies.

Boulay Can Help

Target-Date Funds have become a cornerstone of retirement planning, offering simplicity and adaptability to investors at all stages of their careers. By grasping the nuances of glide paths and the various approaches employed by TDFs, employers can make informed decisions on their plan’s investment lineup and help their employees secure their financial future.

For those interested in learning more or seeking guidance with their employer 401(k) plan, Boulay’s retirement plan advisors are here to help. Connect with us today to learn how we’re dedicated to helping you get there.

Investment Advisory Services offered through Boulay Financial Advisors, LLC a SEC Registered Investment Advisor. Certain Third Party Money Management offered through Valmark Advisers, Inc. a SEC Registered Investment Advisor. Securities offered through Valmark Securities, Inc. Member FINRA, SIPC

Boulay PLLP and Boulay Financial Advisors, LLC are separate entities from Valmark Securities, Inc. and Valmark Advisers, Inc. Prime Global is not affiliated with Valmark Securities, Inc. and Valmark Advisers, Inc.