Executive Summary:

-

-

-

- The FASB’s new accounting standard on the accounting for credit losses (ASU 2016-13 or “CECL”) is effective on January 1, 2023 for non-public companies with calendar year ends.

- The new standard is expected to accelerate the recognition of credit losses. The new standard requires companies to recognize the full lifetime expected credit losses upon the initial recognition of a financial asset that is within the scope of the standard. This differs from the incurred loss model under current GAAP whereby losses are not recognized until they become probable.

- The new standard must be applied to most financial assets carried at amortized cost, including trade accounts receivable.

- The new standard requires companies to group its in scope assets into “pools” and apply an acceptable methodology to each pool to determine the amount of credit loss that needs to be recognized upon adoption and at the end of each reporting period.

- The new standard requires additional disclosures upon adoption and on an ongoing basis in the financial statements, and will require new processes, procedures and internal controls over financial reporting to be developed and applied related to the application of the standard.

-

-

Introduction to the Standard

As a result of the global financial crisis in 2008, the Financial Accounting Standards Board (“FASB”) launched a project to improve the reporting of credit losses. The criticism of the existing “incurred loss” model was that it delayed the recognition of known credit loss exposures until the threshold of “probable” was met. Further, it only considered past events and current conditions in measuring the incurred loss. The result was that users of the financial statements were not provided with timely and relevant information regarding a company’s exposure to credit losses.

Accounting Standards Update (“ASU”) 2016-13 – Measurement of Credit Losses, and subsequent ASUs, which have been collectively added to the Accounting Standards Codification (“ASC”) as ASC 326 – Financial Instruments – Credit Losses, is the end result of the FASB’s project to address the issues with the previously existing standard. Under the new Current Expected Credit Losses model, commonly referred to as “CECL”, the full lifetime expected credit losses on financial assets are recognized upon the initial recognition of an asset that is within the scope of the standard. The new standard replaces the incurred loss model that recognized losses when a probable threshold was met. The new standard broadens the information that a company must consider in developing its expected credit loss estimate to include forecasted information over the life of the asset, in addition to historical information and current conditions. The use of forecasted information incorporates more timely information in the estimate of expected credit losses, which will be more decision useful to the users of the financial statements. The impact of the CECL standard is that expected credit losses will generally be recognized in a company’s financial statements earlier than under the previous model and expanded disclosures will be required.

The new standard is far reaching and will impact all companies that have trade accounts receivables, contract assets from revenue transactions, financing receivables and loans, and investments in debt securities classified as held-to-maturity and available-for-sale. The standard also impacts companies with reinsurance receivables, receivables that relate to repurchase agreements / securities lending agreements and off-balance sheet credit exposures.

The purpose of this article is to provide an overview of the CECL accounting and reporting requirements under US GAAP.

Companies Impacted / Scope

The short answer to the question of which companies are impacted by this new standard is, nearly all companies are impacted. Yes, the accounting change is particularly impactful to companies / institutions with significant lending activities or investments in debt securities, but any company that has assets on its balance sheet that are measured at Amortized Cost are also impacted.

Assets Measured at Amortized Cost include:

- Receivables that result from revenue transactions (including Contract Assets)

- Financing Receivables / Loans

- Held-to-maturity debt securities

- Reinsurance receivables that result from insurance transactions

- Receivables that relate to repurchase agreements and securities lending agreements

Companies that have any of the following other assets on (or off*) their balance sheet are also impacted:

- Available-for-Sale debt securities

- Net investments in leases recognized by a lessor

- Off-balance-sheet credit exposure related to loan commitments, standby letters of credit, financial guarantees not accounted for as insurance, and other similar off balance sheet instruments.

The CECL standard will require management to make new judgements and calculations when measuring expected credit losses. The standard will necessitate reconsideration and changes to accounting polices, processes and internal controls. New information may need to be collected and IT systems may need to be modified to capture additional data to support the accounting and disclosure requirements.

How the Model Works

The new standard is called the Current Expected Credit Loss (CECL) model because it requires making an estimate of the total expected credit losses that will be incurred on an asset over the entire life of the asset as of (current with) the date that the asset is initially recognized. The following are key aspects / considerations in establishing a CECL model:

- Flexibility in Methodology – There is flexibility within the standard regarding what methods can be used to establish the expected credit loss estimate. The different methods that can be applied are described in a subsequent section. The different methods take into account both internal and external information and include both quantitative and qualitative factors. Use of professional judgement is key in determining the appropriate method and relevant information to be utilized based on each company’s specific facts and circumstances.

- Pooling – The standard requires that a company estimate expected credit losses on a collective (pool) basis for assets with similar risk characteristics. Examples of risk characteristics (non-exhaustive) used to create pools include; payment terms, customer type / size, geography (domestic vs foreign), industry, age / aging, internal or external credit risk score / rating, and historical or expected credit loss patterns. If a financial asset does not share risk characteristics with other financial assets, than the asset is evaluated on an individual basis. In addition, a company must evaluate at each reporting period if a revision of pools is necessary due to a change in the risk characteristics of financial assets that are within the existing pools.

- Contractual Term – The standard requires the company to estimate expected credit losses over the financial asset’s contractual term. The determination of the contractual term will impact the size of the allowance for credit losses. In general, longer contractual terms will result in a larger allowance for credit losses.

- Historical Losses are the Starting Point, but not the end – Historical loss experience is typically the starting point in the analysis. However, adjustments must be made to the historical experience to take into account:

- Asset / Pool specific risk characteristics

- Current conditions; both internal / company specific and external economic considerations

- Reasonable and supportable forecasts of future conditions / losses. If a company is not able to make or obtain reasonable forecasts over the entire life of the asset, it is required to estimate expected losses over the life of the asset not covered by the forecast using an approach that reverts back to historical credit loss information. This may be the case for financial assets with multiple year contractual terms.

- Allowance for Credit Losses for Available-for-Sale Debt Securities – The new standard replaces the Other-Than-Temporary-Impairment (“OTTI”) model under prior GAAP, but it retains the OTTI model’s fundamental nature in that it only recognizes credit losses once securities become impaired and the assessment of impairment is at the individual security level. The new standard differs from current GAAP in the following ways:

- Credit losses are recognized through an allowance account and subsequent reversals of the allowance account are recognized within income in the period in which they occur.

- Credit losses are limited to the difference between the security’s amortized cost and its fair market value.

- The evaluation does not consider 1) length of time fair value has been less than amortized cost, 2) changes in fair value after the reporting date, or 3) historical or implied volatility of fair value.

Impact to the Financial Statements

Assets Measured at Amortized Cost

- Balance Sheet – Measured at the net amount expected to be collected. The allowance for credit losses is a contra-asset account that is deducted from the amortized cost basis of the financial asset(s) to present the net carrying value at the amount expected to be collected on the financial asset(s). This presentation is consistent with the presentation for Accounts Receivable under previous GAAP. This method is now applied to all assets measured at Amortized Cost.

- Statement of Operations – Reflects the measurement of credit losses for newly recognized financial assets, plus increases or decreases in expected credit losses that have taken place during the period related to existing financial assets. The expected credit losses on newly recognized financial assets and any changes in expected credit losses for existing financial assets are recognized as a component of operating expense, similar to current GAAP.

Available-for-Sale Debt Securities

- Balance Sheet – Credit losses on available-for-sale debt securities should be measured in a manner similar to prior GAAP. However, the amendments in the updated standard require that credit losses now be presented as an allowance rather than as a writedown.

- Statement of Operations – The allowance approach is an improvement to prior GAAP because a company will be able to record reversals of credit losses (in situations in which the estimate of credit losses declines) in current period net income, which in turn should align the statement of operations recognition of credit losses with the reporting period in which changes in credit risk occur. Prior GAAP prohibits reflecting those improvements in current period earnings.

The above discussion on the impact to the financial statements is over major asset categories that are expected to impact the majority of non-public companies. Additional specific requirements and accounting treatments exist for other asset categories / transaction types, including 1) Assets Purchased with Credit Deterioration, 2) Recoveries of Assets Previously Written off and 3) Troubled Debt Restructurings, to name a few. You are encouraged to reach out to your Boulay client service team to assess financial statement impacts that are specific to your company.

Methods to estimate expected credit losses

As stated above, there is flexibility within the standard regarding what methods can be used to establish the expected credit loss estimate. The guidance from the standard specifically reads:

ASC 326-20-30-3

The allowance for credit losses may be determined using various methods. For example, an entity may use discounted cash flow methods, loss-rate methods, roll-rate methods, probability-of-default methods, or methods that utilize an aging schedule. An entity is not required to utilize a discounted cash flow method to estimate expected credit losses. Similarly, an entity is not required to reconcile the estimation technique it uses with a discounted cash flow method.

ASC 326-20-55-7

Because of the subjective nature of the estimate, this Subtopic does not require specific approaches when developing the estimate of expected credit losses. Rather, an entity should use judgment to develop estimation techniques that are applied consistently over time and should faithfully estimate the collectability of the financial assets by applying the principles in this Subtopic. An entity should utilize estimation techniques that are practical and relevant to the circumstance. The method(s) used to estimate expected credit losses may vary on the basis of the type of financial asset, the entity’s ability to predict the timing of cash flows, and the information available to the entity.

The key takeaway from this guidance is that a company should choose a method(s) / model(s) that are practical and relevant to their company and the company’s specific asset(s) that requires a CECL reserve. A company can (and should) use different models for different classes of assets that are on their balance sheet.

For example, the best method to be utilized by a company to estimate expected credit losses on its trade accounts receivable may be a method that utilizes an aging schedule. The same company could use a discounted cash flow method for its available for sale securities to determine the best estimate of the present value of cash flows expected to be collected. If this same company were to issue debt securities, it could use a loss rate method to estimate its necessary CECL reserve.

The key aspect to remember when applying models that are based on historical information, like an aging schedule or a loss rate method, is that historical information is only the starting point. The model must take into account current conditions and reasonable and supportable forecasts for the future. In addition, when using historical information and forecast information, a company must consider the relevant periods to include in the analysis. Assets with a longer contractual term will require a longer historical lookback and a forecast covering the term of multiple year contracts / arrangements. Conversely, trade receivables could require a shorter historical period that is representative of expected future losses and a shorter forecast period. The following is an example using an aging schedule and trade accounts receivable. Trade accounts receivable has been selected for this example as it is applicable to the majority of Boulay clients.

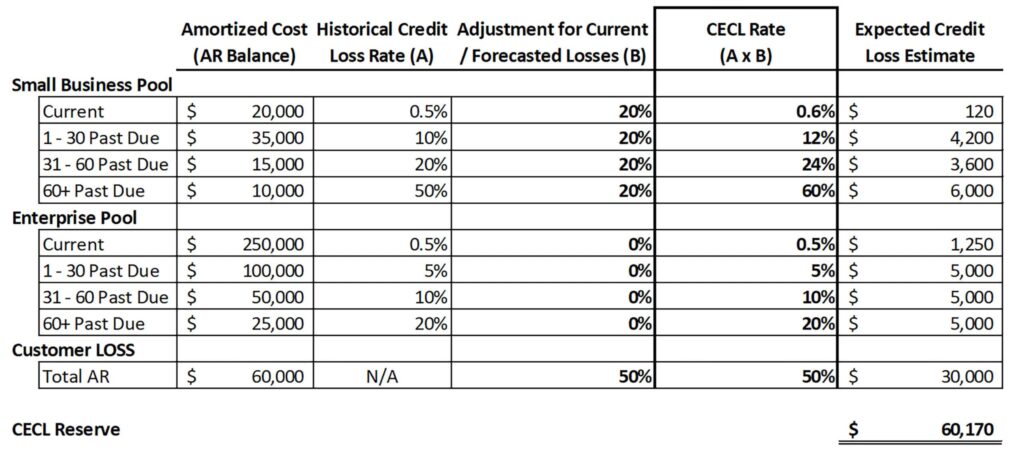

Relevant facts for Company XYZ in the example:

- Company XYZ has two classes of customers 1) small business and 2) enterprise

- The historical rate of loss by class of customers over the past two years (which is considered appropriately representative) is:

- Small business: 0.5% on current; 10% on 1-30 days past due; 20% on 31-60 day past due; 50% on aged past 60 days due

- Enterprise: 0.5% on current; 5% on 1-30 days past due; 10% on 31-60 days past due; 20% on aged 60 days past due

- Current economic conditions are negatively impacting small businesses, and the condition is expected to worsen in the coming months. Enterprise businesses are not expected to be impacted by these negative economic impacts

- As a result of the current and forecasted economic conditions, company XZY estimates, that credit losses on trade receivables with small businesses will increase by 20% and that the condition is expected to persist into the foreseeable future.

Considering the above assumptions, Company XYZ would properly determine that it has Eight Pools of receivables based on the different risk characteristics for 1) small business vs 2) enterprise customers and the four aging buckets for each of these classes of customer. However, during the credit loss analysis performed for 12/31/23, Company XYZ identifies from a business journal article that one of its enterprise customers (Company LOSS) is in significant financial distress and the condition is expected to continue for at least the next 9 months. Thus, Company LOSS no longer shares the same economic characteristics of the other enterprise customers and must be separately evaluated. Credit losses on Company LOSS are expected to be 50% on all outstanding receivable balances, and thus the historical credit loss rate and aging are no longer relevant characteristics as relates to customer LOSS, only the future expectations are relevant.

Aging at 12/31/23

The process undertaken by Company XYZ in the above example 1) properly separates its trade receivables into separate pools sharing similar characteristics, 2) applies historical credit loss information as the starting point, and 3) takes into account current / forecasted economic conditions in determining its CECL reserve amount. Specifically, although the Company may have robust processes for establishing reserves based on historical information, this historical information does not take into account any potential future impact on receivables (even current receivables) that may be uncollectable because of the economic conditions that will be impacting small business in the example. Thus, the reserve needs to be increased for the small business pools based on estimated / forecasted future losses for receivables currently on the balance sheet due to worsening economic conditions. In specific regard to Customer LOSS, historical loss information is no longer relevant to the analysis based on Customer LOSS’s significant current distress, so it is replaced in its entirety by the current / forecasted estimate of loss. The resulting CECL reserve that would be recorded is $60,170, as illustrated above.

The above example has been presented as it is considered to be one of the most applicable to Boulay’s clients. Other models will be more appropriate to different asset classes and companies with different fact patterns. Please consult with your Boulay client service team to assist in determining methods / models that are most appropriate for your specific asset groups.

Final note on the example. Many companies currently have an accounts receivable process that uses aging buckets and historical loss information to establish an allowance for doubtful accounts reserve. This is a great starting point, but it is just a starting point. Even before consideration of current / future aspects of the model, additional rigor needs to be applied to justifying credit loss history related to the individual aging buckets / pools and the historical period used to establish the credit loss history. For example, using credit loss history over the past three years would not be appropriate if the past six months of historical information shows a distinct change in credit losses. Similarly, using a blended “probable” loss rate across multiple buckets is not appropriate because it does not take into account the different risk characteristics that exist for receivables from different classes of customers, geographies, etc., or different risks as the receivables age. The historical model may also be based on the “probable” threshold, which is too high a threshold under CECL. Documentation / justification of assumptions is key. We recommend discussion of assumptions to be used in models with the Boulay client service team in advance of year-end so we can provide timely comments / recommendations on your models / assumptions.

Adoption Method

The new standard is to be adopted using the Modified-Retrospective Approach as of the beginning of the first reporting period in which the guidance is effective **. For companies with calendar year ends, the effective date is January 1, 2023. In the year of adoption, the cumulative effect adjustment of the transition from existing GAAP to the new CECL model is recorded as an adjustment to retained earnings with no adoption impact to the Statement of Operations / Net Income. For example, if the allowance for credit losses under previous GAAP was $1,000 and the determined loss under the CECL model is $1,500, the $500 additional reserve is recorded as a reduction to retained earnings on January 1, 2023 (for calendar year reporters) and the statement of Operations for 2023 is not negatively impacted by the additional $500 reserve created from adoption. This retrospective adoption method is Modified, because typically under a retrospective adoption retained earnings as of the earliest period presented in the financial statements would be adjusted (this would call for an adjustment to retained earnings as of January 1, 2022 for calendar year 2023 adopters). Under the Modified approach, only the current reporting period is impacted (January 1, 2023 retained earnings).

The Modified-Retrospective transition model under the new standard represents a soft landing for companies upon adoption and encourages a thorough analysis and recording of expected credit losses at adoption. For example, if a company were to take an aggressive approach in its analysis that downplayed current economic conditions and forecasts for the future with a resulting small CECL reserve, when actual losses / non-collections in subsequent periods are in excess of the opening reserve, the Statement of Operations / Net Income would be negatively impacted by the amount that actual non-collections exceed the reserve. Alternatively, if a company undertakes a thorough and supported analysis, using an appropriate model, and records a larger reserve upon adoption (with no adoption impact to the Statement of Operations), when amounts reserved for at adoption are ultimately uncollectible, the write-off is against the reserve and does not impact that Statement of Operations / Net Income.

** A prospective transition approach is required for debt securities for which an OTTI had been recognized before the effective date. If this situation impacts your company, please consult with a member of your Boulay client service team.

Subsequent Accounting

After establishment of the CECL reserve as of January 1, 2023 (calendar year companies), subsequent non-collections are written off against the balance sheet reserve. Companies will be required to reassess their required CECL reserve each reporting period, with adjustments up or down typically flowing through the statement of operations. Because actual write-offs during a period are recorded against the reserve (reducing the reserve amount), the assumption is that period end reassessments of the required CECL reserve will result in an increase / replenishment of the reserve to take into account estimated credit losses on new assets acquired in the period, as well as any new negative collection evidence related to existing assets / asset pools. The increase to the reserve amount will flow through the statement of operations. However, in the case of improved economic conditions, forecasts or other company specific factors, it may be determined that a reduction to the reserve is required, with accompanying benefit to the statement of operations.

Disclosure Requirements

The objective of the CECL standard is to provide users of the financial statements with timely and decision useful information regarding a company’s credit risks. The standard requires both qualitative and quantitative disclosures regarding the following:

- The credit risk inherent in the company’s financial asset portfolio and how management monitors the credit quality of those financial assets

- The company’s estimate of expected credit losses

- Changes in the estimate of expected credit losses that have taken place during the period

All disclosures are required on a disaggregated basis by either portfolio segment or class of financial asset. Specific disclosure requirements exist for the following (if applicable):

- Credit quality information; including a description of the credit quality indicator(s) and the amortized cost basis by credit quality indicator

- Allowance for credit losses; including methods and information used to determine credit loss allowances and any circumstances that caused changes to estimates

- Rollforward of allowance for credit losses

- Past-due status

- Nonaccrual status

- Information on financial assets purchased with credit deterioration

- Collateral-dependent financial assets

- Off-balance sheet credit exposures

Next Steps

We hope this article has provided a helpful summary of the new accounting requirements for credit losses under ASC 326 / “CECL”. This summary has addressed the topics that are expected to impact the majority of non-public companies that will be required to adopt CECL. The full standard is quite comprehensive and addresses additional aspects / specific credit loss situations for specific assets that have not been addressed in this summary. To better understand how this standard will impact your financial statements, please reach out to a member of your Boulay client service team, or contact us at 952.893.9320 or learnmore@boulaygroup.com. We look forward to assisting you with your adoption of this standard.