Many of us go about saving for the future with our best intentions and best guesses and hope that we are doing the right thing. Here is a thoughtful and thorough “order of operations” on how to save.

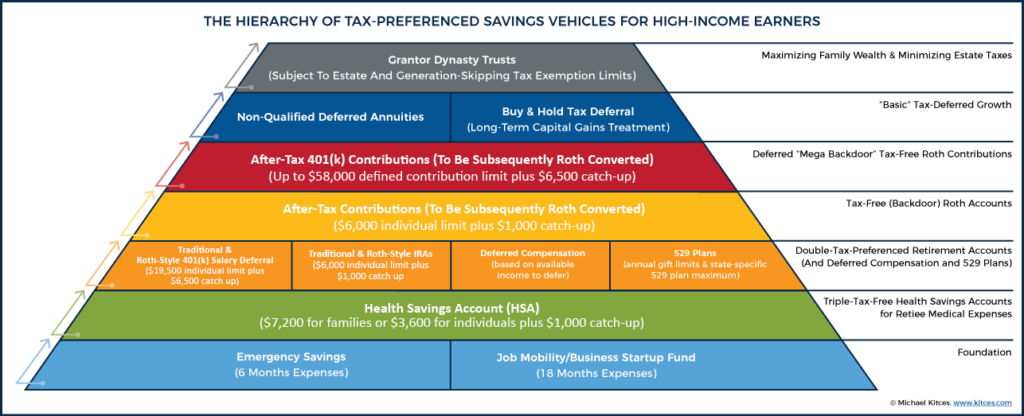

The foundation is cash. An emergency fund is central to ensuring your financial house stays standing. A common rule of thumb is to have 3-6 months in cash at the ready to cover your “needs.” Once you have filled up the first tier, you are ready to move to the next level.

Most people get the next level wrong. Health savings accounts (HSA) are the best place to save and invest your money due to the extraordinary tax benefits You a triple tax benefit of tax-deductible contributions, tax deferred growth and tax-free distributions.

Once your HSA is maxed out each year, we move onto tier three, which is where accounts provide a double tax benefit of either tax-deductible contributions and tax-deferred growth (IRAs) or tax-deferred growth and tax-free distributions (Roths). Typically, one can move from left to right, which is to first max out your 401K, then spill over into your individual retirement account (IRA/Roth), Deferred Comp options through work and finally educational accounts, such as 529 plans.

The fourth tier are for those high-income earners who normally could not get deductible IRA contributions nor direct Roth contributions. They can deploy the back-door Roth strategy.

The fifth tier is for those who have access to the Mega Back Door Roth 401k strategy.

A married couple typically has about $60,000 – $130,000 of capacity to fill up the tax-advantaged buckets thus far amongst their HSA, 401Ks and IRAs. In most cases, only then would we look to fund the sixth tier, which provides only tax-deferred growth. Commonly, brokerage accounts can defer gains as long as appreciated investments are held and not sold. The use of tax deferral tools, such as Investment Only Variable Annuities, can be a good option.

Finally, if one’s wealth is larger than what may be needed during one’s lifetime, estate tax planning strategies top off the mix.

If you are saving for retirement, we can help you identify the right amount to save and then a flexible, tax efficient plan on how best put your money to work. Contact a Boulay wealth management advisor today.