Key takeaways

- Asset allocation determines your risk and return profile

- Asset location can enhance tax efficiency

- Asset migration helps your plan evolve over time

- These strategies work together to help improve long-term, after-tax investment results

Asset allocation, asset location and asset migration are three core strategies in wealth management. While they sound similar, each plays a distinct role in helping investors grow wealth, manage risk and reduce the burden of taxes over time.

Understanding how these strategies work together can significantly improve long-term, after-tax investment results.

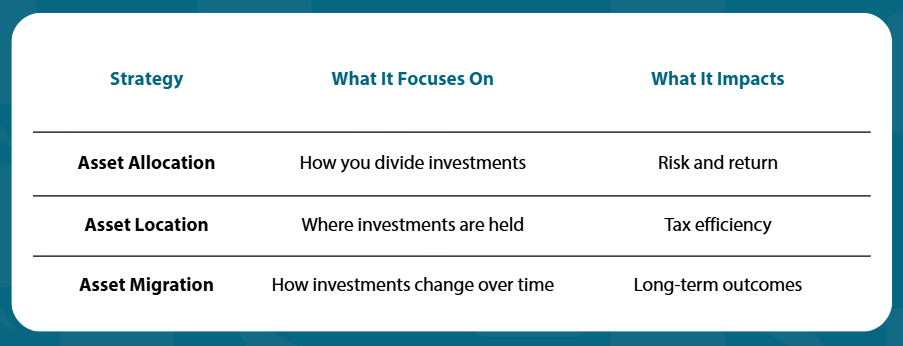

Asset Allocation vs asset location vs asset migration

- Asset allocation is the process of structuring your portfolio to balance growth potential, stability, liquidity and risk.

- Asset location refers to placing investments in the most tax-efficient account type. It focuses on where you hold assets, not what you own.

- Asset migration means strategically moving assets over time between investments, accounts, or tax treatments to support changing financial goals.

What is asset allocation in investing?

Asset allocation is how you divide your investments among major asset classes—typically stocks, bonds and cash (and sometimes real estate or alternative investments).

Research consistently shows that asset allocation is one of the most important drivers of long-term portfolio performance, which is often more impactful than selecting individual securities.

Stocks (Equities)

Offer higher long-term growth potential but come with greater volatility.

Bonds (Fixed Income)

Provide stability and income, typically with lower long-term returns than stocks.

Cash and Cash Equivalents

Offer liquidity and capital preservation, but may lose purchasing power due to inflation over time.

How do you determine the right asset allocation?

The “right” allocation depends on:

- Time horizon

- Risk tolerance

- Income needs

- Overall financial goals

Younger investors often allocate more heavily to stocks because they have time to recover from market fluctuations. Investors approaching retirement may shift toward bonds and cash to reduce downside risk.

Asset allocation should not be static. It should be reviewed periodically and adjusted as market conditions, goals, or life circumstances change.

What is asset location?

Asset location refers to placing investments in the most tax-efficient account type. It focuses on where you hold assets, not what you own.

Different account types receive different tax treatment:

Types of Investment accounts

Taxable accounts

Taxes are paid annually on interest, dividends and realized capital gains.

Tax-Deferred Accounts (Traditional 401(k), Traditional IRA)

Contributions may be deductible; investments grow tax-deferred until withdrawal.

Tax-Free Accounts (Roth IRA, Roth 401(k))

Contributions are made with after-tax dollars, and qualified withdrawals are tax-free.

Why Does asset location matter?

Certain investments generate more taxable income than others. For example:

- Bonds and high-turnover funds typically generate ordinary income

- Broad stock index funds and tax-efficient ETFs tend to generate lower taxable distributions

A common strategy is to:

- Place tax-inefficient assets (like bonds) in tax-deferred accounts

- Hold tax-efficient investments in taxable or tax-free accounts

Done properly, asset location can improve after-tax returns without increasing portfolio risk.

What is asset migration in Wealth Management?

Asset migration refers to strategically moving assets over time—between investments, accounts, or tax treatment—to align with evolving financial goals.

It answers the question: When and how should investments change?

Examples of Asset Migration Strategies

- Rebalancing to maintain your target asset allocation

- Gradually shifting toward conservative investments near retirement

- Converting traditional retirement assets to Roth accounts

- Harvesting gains or losses strategically to manage taxes

- Relocating assets between account types for tax efficiency

Why is asset migration important?

Migrating assets thoughtfully helps your strategy adapt without triggering unnecessary taxes or unintended risk exposure.

Poorly timed moves—or reactive decisions during market volatility—can undo years of disciplined investing. Strategic asset migration balances:

- Market risk

- Tax impact

- Cash flow needs

- Long-term wealth objectives

How do Asset allocation, asset location and asset migration compare?

How do asset allocation, location and migration work together?

These three strategies are interconnected:

- Asset allocation determines your risk and return profile.

- Asset location enhances tax efficiency.

- Asset migration helps your plan evolves over time.

Together, they form the foundation of disciplined, long-term wealth management—often delivering more value than attempting to outperform the market through stock picking or market timing.

Build a strategy designed for Long-Term Success

Every investor’s financial picture is different. A coordinated approach to asset allocation, asset location and asset migration can help improve outcomes while managing risk and taxes efficiently.

To explore how these strategies may apply to your personal financial situation, connect with a Boulay Wealth advisor for guidance tailored to your goals.

frequently asked questions about tax-efficient wealth management

what is the difference between asset allocation, asset location and asset migration?

Asset allocation determines how your investments are divided across asset classes. Asset location focuses on where those investments are held for tax efficiency. Asset migration is how those investments are adjusted over time as your goals, tax situation, or risk tolerance change.

Why is asset allocation important?

Asset allocation helps shape your portfolio’s risk and return profile. It can influence how much growth potential, stability and income your investments provide over time.

Why does asset location matter for taxes?

Asset location matters because different accounts are taxed differently. Placing certain investments in the right account type can help reduce taxes and improve after-tax returns.

What is an example of asset location?

One example is holding tax-inefficient assets, such as bonds, in tax-deferred accounts while holding more tax-efficient investments, such as broad stock index funds or ETFs, in taxable accounts.

What is an example of asset migration?

Asset migration may include rebalancing a portfolio, gradually shifting toward more conservative investments near retirement, converting traditional retirement assets to Roth accounts, or harvesting gains and losses strategically.

How often should these strategies be reviewed?

These strategies should be reviewed periodically, especially when market conditions, financial goals, income needs, tax laws, or life circumstances change.

How do these strategies work together?

Together, asset allocation, asset location and asset migration help create a coordinated investment strategy designed to manage risk, improve tax efficiency and support long-term wealth goals.

This material is for informational purposes only and is not intended to provide specific advice or recommendations for any individual nor does it take into account the particular investment objectives, financial situation or needs of individual investors. Past performance does not guarantee future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss.

Investment Advisory Services offered through Boulay Financial Advisors, LLC a SEC Registered Investment Advisor. Certain Third Party Money Management offered through Valmark Advisers, Inc. a SEC Registered Investment Advisor. Securities offered through Valmark Securities, Inc. Member FINRA, SIPC

Boulay PLLP and Boulay Financial Advisors, LLC are separate entities from Valmark Securities, Inc. and Valmark Advisers, Inc. Prime Global is not affiliated with Valmark Securities, Inc. and Valmark Advisers, Inc.