Congress has officially passed President Donald Trump’s sweeping new tax bill, bringing major changes to many Americans’ finances. Most notably, the GOP’s “One Big Beautiful Bill” extends, enhances, and adjusts many provisions from the 2017 Tax Cuts and Jobs Act (TCJA). Unlike the TCJA, which was signed into law at year-end, this bill gives taxpayers a valuable mid-year planning window to act before the changes take effect for the 2025 tax year.

This article highlights the key changes affecting individual taxpayers, explains how high-income earners may be impacted by new phaseouts, and outlines what you can do now to prepare.

Key Points:

- President Trump signed his party’s tax and spending package into law on Friday, July 4, extending sweeping tax cuts and bringing changes to many Americans’ finances

- Key among the changes is making permanent and expanding the 2017 TCJA tax cuts, while adding a ‘bonus’ deduction for seniors intended to offset Social Security taxes

- For a summary of the changes compared to current law, see table below

Standard Deduction and Tax Brackets

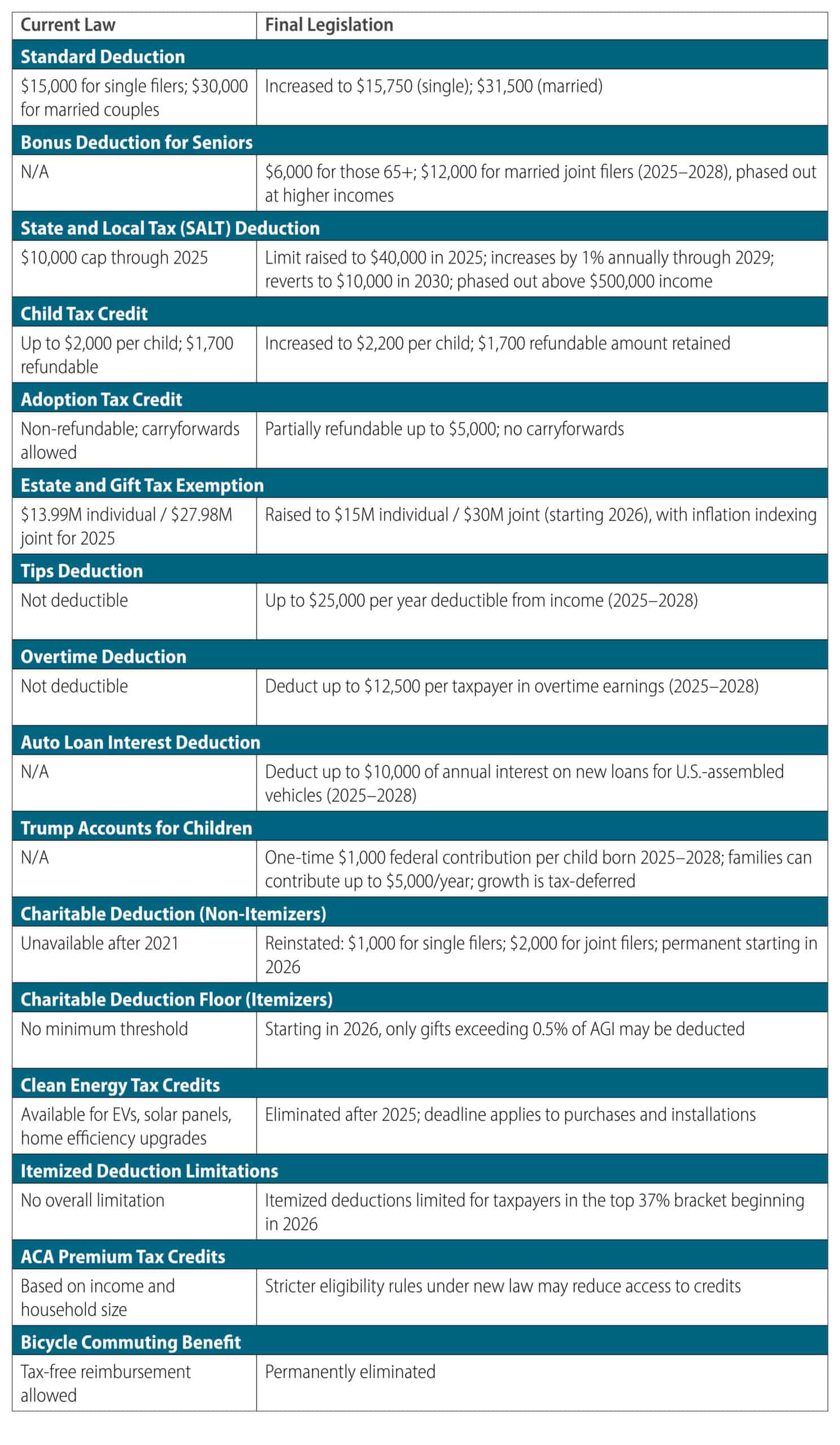

One of the most prominent changes is the permanent increase in the standard deduction, now set at $15,750 for single filers and $31,500 for married couples filing jointly, effective in 2025. These amounts will continue to be adjusted for inflation in future years.

The seven tax brackets from the TCJA remain in place, with a top marginal rate of 37% and a bottom rate of 10%.

Enhanced Benefits for Older Adults

Taxpayers aged 65 and older will benefit from a significantly expanded deduction—an additional $12,000 for those filing jointly and $6,000 for most single filers—from 2025 through 2028. This is above and beyond the previous senior standard deduction increase of $3,200 for joint filers and $2,000 for single filers. These new deductions are phased out for incomes over $75,000 (single) and $150,000 (married filing jointly), making income planning especially important in retirement.

Child and Adoption Tax Benefits

Beginning in 2025, the Child Tax Credit increases to $2,200 per child and is now a permanent part of the tax code. The refundable portion remains $1,700, providing meaningful support for families with qualifying dependents. These amounts will continue to be adjusted for inflation in future years.

In a win for adoptive families, the adoption tax credit will now be partially refundable—up to $5,000, adjusted annually for inflation. However, unused amounts cannot be carried forward to future years, so strategic timing is key.

SALT Deduction Temporarily Expanded

The state and local tax (SALT) deduction cap rises to $40,000 in 2025, with 1% increases through 2029 before reverting back to $10,000 in 2030. This deduction phases out for incomes above $500,000, whether you file single or jointly—meaning the value diminishes at higher income levels.

Estate and Gift Tax Exemption Increased

High-net-worth individuals should take note: the lifetime estate and gift tax exemption will increase to $15 million for single filers and $30 million for joint filers, starting in 2026 with annual inflation adjustments going forward. This creates new planning opportunities for wealth transfer and gifting strategies.

New Deductions for Working Individuals

Several new deductions aim to provide relief to middle-income earners between 2025 and 2028. Each of these is an above-the-line deduction (meaning it’s available regardless of whether a taxpayer itemizes deductions):

- Tips: In certain industries, deduct up to $25,000 of tip income per year

- Overtime: Deduct up to $12,500 per taxpayer in qualified overtime pay

- Auto Loan Interest: Deduct up to $10,000 in interest for certain U.S.-assembled vehicles

Each of these deductions is subject to income-based phaseouts, so taxpayers approaching high-income thresholds may need to plan carefully.

Itemized Deduction Limits

Also beginning in 2026, limits on itemized deductions will be reintroduced, using a new formula that replaces the prior “Pease rule” for high-income taxpayers. This change may increase the marginal cost of additional income and reduce the value of itemizing at higher income levels.

Charitable Deductions Return—With a Caveat

For the first time since 2021, non-itemizing taxpayers can again deduct charitable gifts—$1,000 for single filers and $2,000 for married couples. This provision becomes permanent in 2026.

However, beginning in 2026, itemizers will only be able to deduct charitable contributions to the extent they exceed 0.5% of adjusted gross income (AGI). This new “floor” may reduce the benefit of charitable gifts for higher earners.

“Trump Accounts” for Newborns

Parents of children born between 2025 and 2028 can open new “Trump Accounts”—tax-deferred investment accounts seeded with a $1,000 government contribution. Families may add up to $5,000 annually, and growth is tax-deferred. Withdrawals in young adulthood are taxed like a brokerage account.

Clean Energy Incentives Phased Out

Taxpayers considering green upgrades should act quickly. Tax credits for electric vehicles, energy-efficient home improvements, and residential solar installations will expire after 2025, removing a popular incentive for sustainability-focused investments. Individuals need to make car purchases by the end of September and install solar panels by the end of December to qualify for tax credits.

Business Owner Highlights

The bill also brings two key wins for small business owners and pass-through entities:

- Pass-Through Business Deduction (Section 199A): The deduction for qualified business income is now permanent. The income phaseouts are increased slightly for tax years after 2025.

- Pass-Through Entity (PTE) Exclusion Strategy: The strategy allowing businesses to pay state taxes at the entity level—providing a workaround to the SALT deduction cap for owners—remains in place.

Policy Changes Beyond the Tax Return

A few provisions in the new bill fall outside the tax return—but may still affect your financial situation:

- Student Loans: New annual and lifetime borrowing limits will be introduced, and income-based repayment plans will consolidate into two options by mid-2026

- Medicaid and Food Stamps: Non-disabled adults without dependents must meet new work or volunteer requirements (20 hours/week)

- Affordable Care Act (ACA) Premium Tax Credits: Eligibility is narrowed under the new rules, potentially increasing insurance costs for some marketplace enrollees

Planning Ahead: What Should You Do Now?

With many of these provisions taking effect in 2025, now is the ideal time to review your financial picture and determine your next moves:

- Consider the impact of income thresholds and deduction phaseouts

- Reassess your retirement contribution strategy (Roth vs. pre-tax)

- Maximize charitable giving and evaluate bunching strategies

- Plan around estate tax changes and business income deductions

While the deductions introduced in this bill are more generous for some taxpayers, new phaseouts tied to income levels mean that earning just a bit more could reduce or eliminate certain tax benefits. That makes income timing and deduction strategy more important than ever. Knowing when to accelerate deductions or defer income—or vice versa—can make a meaningful difference in your tax outcome. Decisions around pre-tax vs. Roth retirement contributions, charitable giving strategies, and when and how to recognize investment income (through portfolio distribution planning and asset location) will play a key role in minimizing your overall tax burden.

Boulay Can Help

Whether you’re nearing retirement, running a business, or raising a family, the decisions you make this year can have long-term impact. Boulay’s wealth and tax advisors can help identify your optimal planning opportunities and avoid hidden tax cliffs.

Every taxpayer’s situation is different, but everyone can benefit from a clear understanding of these updates and a strategy tailored to their goals. Contact your Boulay advisor or connect with us today to schedule a personalized review.

2025 Tax Law Changes: Side-by-Side Comparison